Share Pooling Crypto: How to Calculate Crypto Gains in the UK

The tax deadline is coming up, and you’re still unsure how to accurately calculate your crypto gains to report to HMRC. We’ve got you.

HMRC makes one thing clear: Crypto investors like you should be using the share pooling cost basis method.

This guide will let you know what share pooling actually is when it’s out of bed and how you can use it to easily calculate your crypto capital gains.

Share pooling rules

HMRC calls pooling the Section 104 Rule, but for everyone else, it’s known as an average cost basis method.

Here’s how it works: When you have identical assets, you pool those assets and take an average cost basis for each one of those pools.

You need to do this for each kind of crypto asset you own. You have a pool (section 104 pool) for ETH, BTC, DOGE, and so on.

Example:

You have 3 ETH with a cost basis of £2,000, £800, and £1,500

Add up each cost basis for a total of £4,300

Divide the total by the number of coins/tokens held in that pool – in this case, 3

You get an average cost basis of £1,433.

Anytime you dispose of ETH by selling, swapping, spending, or gifting it (unless it’s to your spouse), you’d use this cost basis to calculate any capital gain or loss to report to HMRC.

Crypto wash sales

The thing about the average cost basis is that it can be easily manipulated.

Shady investors can:

Purchase assets at a much lower cost to artificially reduce their cost basis.

Sell them quickly to reduce their gains and tax bill.

Then buy back assets quickly after to continue holding long-term investments.

This is known as a Wash Sale, and HMRC doesn’t approve…at all.

That’s why they introduced very specific cost basis rules to define how you calculate the average cost of assets, including the Section 104 Rule.

How to calculate crypto taxes (using the share pooling cost basis method)

You need to work through three rules, in this exact order, to calculate your crypto taxes:

The same-day Rule – TCGA92/S105 (1)(a)

The 30-day rule (Bed and Breakfasting Rule) – TCGA92/S106A (5) and (5a)

Section 104 Rule – s.104 pool

Let’s tackle them one by one.

Same-day Rule

The Same-day Rule comes first.

If you buy and sell coins on the same day, you’ll use the cost basis from the tokens or coins you purchased that day to calculate your subsequent gain or losses.

HMRC see tokens bought and sold on the same day (such as buying some in the morning and selling them that same evening) as a single transaction.

You use the average cost basis and average sale price for all your tokens bought and sold on that day to calculate your gain or loss.

If you sold or traded more tokens than you bought that day, you’ll move on to the Bed and Breakfasting Rule.

Example:

On 15 July 2025, Elizabeth sold 0.5 BTC.

On the same day, she bought 0.3 BTC.

That leaves 0.2 BTC unmatched.

If Elizabeth bought 0.2 BTC back within 30 days (from the 15th July), she would be subject to the Bed and Breakfasting Rule.

Bed and Breakfasting Rule

More commonly (and unexcitingly) known as the CGT 30-Day Rule, the Bed and Breakfasting Rule says that if you sold tokens and then repurchased tokens of the same kind within 30 days, those repurchases must be used as the cost basis to calculate your gains or losses.

If you sell and repurchase the same tokens within a 30-day period, you’ll use the FIFO (First In, First Out) cost basis method to calculate your cost basis for disposals from that period (not the cost basis from your Section 104 pool).

Without the 30-Day Rule, investors could sell at a loss, buy back instantly, and walk off with tax-free gains. HMRC caught on, so this rule makes that a lot more difficult, as the investor will not be able to buy the assets back within the 30 days if they want to use the losses.

If you sold more tokens than you bought within the last 30 days, you’ll move on to the Section 104 rule.

Section 104 Rule

We’ve discussed this one before, but in case you skipped it: Section 104 Rule, also known as pooling, says investors should use the average cost basis method to calculate an average cost for a given pool of assets.

The formula is still:

Total cost of the pool / Total number of tokens = Average cost basis

You then use this cost basis to calculate subsequent gains and losses.

Remember: Any disposal of crypto is subject to the Same Day and Bed and Breakfasting rules:

Selling crypto

Crypto-to-crypto trades

Spending crypto

Gifting (except to your spouse or civil partner – love wins, taxes lose)

Let's look at some examples to better understand how each rule works.

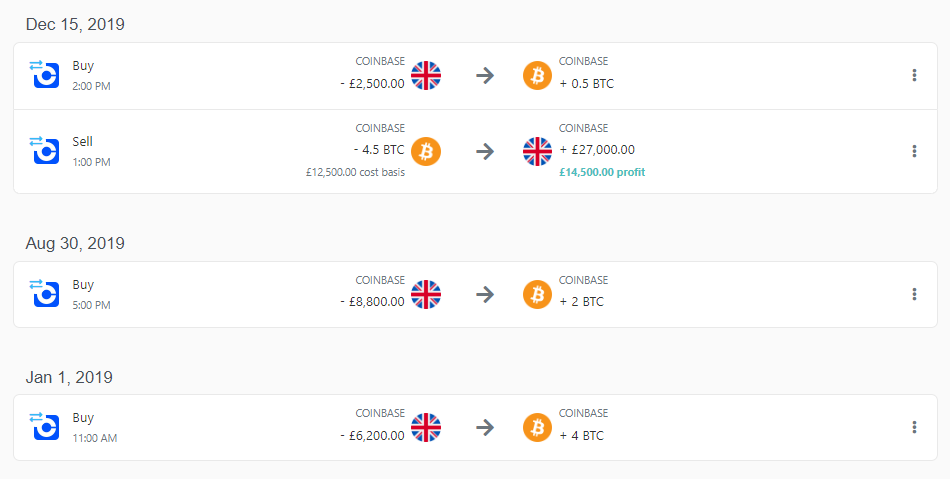

Example 1

Ryan carried out the following transactions for Bitcoin:

1 Jan 2019: Purchased 4 BTC for £6,200

30 Aug 2019: Purchased 2 BTC for £8,800

15 Dec 2019: Sold 4.5 BTC for £27,000

15 Dec 2019: Purchased 0.5 BTC for £2,500

In this example, the disposal is first matched with the purchase made on the same day, then against the share pool.

The main reason why you have to use the 30 day rule is to prevent a practice known as bed and breakfasting where a person sells shares when they are trading at a low price to generate a tax loss and later buys the assets back to maintain his position in that asset. This is also known as a wash-sale as it is not a genuine sale. The 30 day rule makes this much more difficult as the person will not be able to buy the assets back within 30 days if he wants to use the losses.

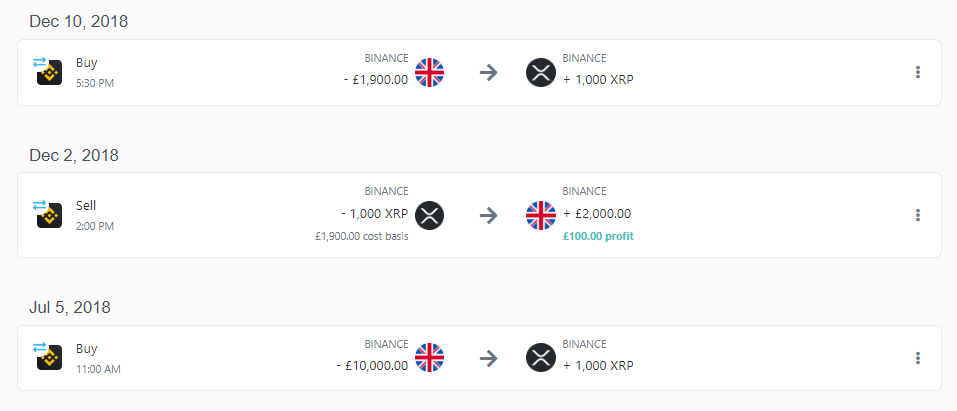

Example 2

Douglas purchased 1,000 XRP on 5 July 2018 for £10,000. The price of XRP has fallen in value, so he would like to establish a capital loss. So, he sells the shares on 2 December 2018 for £2,000 and purchases them back on 10 December 2018 for £1,900.

Douglas’s transactions are caught by the 30 day rule. The disposal on 2 December 2018 will be matched with the purchase on 10 December 2018, and for 2018–19 he will therefore have a chargeable gain of £100 (2,000 – 1,900).

Share pooling rules for cryptoassets for companies

For UK companies, HMRC generally requires cryptoassets to be taxed using share pooling rules under section 104, the same as for individuals.

This means instead of tracking the cost of each individual token, a company groups all tokens of the same type into a single pool. The pool records the total number of tokens held and the total acquisition cost. When more tokens are bought, both totals increase. When some are disposed of, a proportion of the pooled cost is used to calculate the gain or loss for Corporation Tax.

However, not every disposal comes from the main pool. Two matching rules take priority:

First, tokens disposed of are matched with tokens acquired on the same day.

If there are still tokens left to match, the disposal is then matched with tokens acquired within the following 10 days (the “bed and breakfast” rule).

If the disposal is not fully matched under these rules, the remaining amount is taken from the section 104 pool.

Calculate UK crypto taxes with Koinly

We know that if you’re an active investor, you’re probably trading large volumes and could have hundreds, if not thousands, of transactions. And now you’re asking, “How can I apply all these rules with all this data?”

That’s exactly why we developed Koinly, a sophisticated crypto tax software tool that can reliably do all the calculations for you.

Koinly supports the share pooling cost basis method for UK individuals and for companies. You can find this in settings.

Koinly:

Koinly:

Automatically applies Same-Day, 30-Day, and Section 104 rules

Calculates the correct basis for every transaction

Generates your capital gains figure

Produces your UK-specific tax form (including HMRC’s Capital Gains Summary)

All you have to do is head to the tax reports page and download the ones you need.

Hopefully, you now have a better idea of how capital gains are calculated in the UK.

Hopefully, you now have a better idea of how capital gains are calculated in the UK.

If you’re looking for more, check out our expertly curated UK Crypto Tax Guide, which covers the tax rules for different types of crypto transactions as well as ways to reduce your taxes.