How to Report Crypto on Taxes: Crypto Tax Forms 8949 & Schedule D

Navigate how to report your cryptocurrency on taxes confidently with our complete guide on crypto tax forms. From IRS Schedule D to Form 8949 to Schedule 1, we've got you covered with the latest requirements and how to fill out Form 8949 for cryptocurrency with examples, and how to generate your crypto tax forms with Koinly.

Which crypto tax forms do you need?

| Form | Who needs it? | What's included? | View form |

|---|---|---|---|

| Form 8949 | Anyone with capital gains or losses from crypto | Report each disposal of crypto | Form 8949 |

| Schedule D | Anyone with capital gains or losses from crypto | Report your net gain or loss from crypto | Schedule D |

| Schedule C | Self-employed investors earning income from crypto | Report gross income and profit from crypto | Schedule C |

| Schedule 1 (Form 1040) | Anyone with additional income from crypto | Report crypto income in part 1, line 8 | Schedule 1 |

| Form 1099-DA | Investors receiving a digital asset 1099 from an exchange or broker. | Transaction data reported directly to the IRS that must be reconciled with taxpayer reporting. | 1099-DA |

We'll cover them one by one, plus how to file with Koinly.

Form 8949

IRS Form 8949 is a supplementary form for the 1040 Schedule D. This form is used to report any disposals of capital assets, in this instance, cryptocurrency, and it's been updated for 2026 in light of the 1099-DA forms.

So anytime you’ve ‘disposed’ of crypto by selling it, swapping it, or spending it, you’ll include it on this form. For each disposal, you’ll need the following information:

A description of the asset: for example, 0.5 BTC.

The date you acquired the asset: for example, 15th May 2025.

The date you disposed of the asset: for example, 20th August 2025.

The sale price at fair market value: for example, $30,000.

The cost basis of the asset at fair market value: for example, $20,000 + $50 in transaction fees.

Used if you need to report an adjustment, such as reconciling differences between your own records and what an exchange reports on Form 1099-DA. Common reasons include missing fees, transfers not matched, or brokers using a different cost basis method.

If you enter a code in column (f), you’ll also enter the dollar amount of the adjustment here. This ensures your totals reflect accurate gains/losses and match IRS records.

Your capital gain or loss: for example, $9,950.

How to fill out Form 8949 for cryptocurrency

Form 8949 is split into two parts: short-term and long-term.

In the first section, you’ll fill out your short-term disposals. The second part is your long-term disposals. This applies to any asset you’ve held for more than a year before disposing of it. The latter is taxed at lower rates.

For both sections, you’ll need to fill out your total gains at the bottom of the page. You'll need to calculate your:

Total proceeds

Total cost basis

Total gain or loss

You’ll need to do this for both sections for your short-term and long-term gains. You’ll also need to check another couple of boxes on this form, corresponding with your 1099-DA forms (or use tax software that'll do it for you).

For part 1 (short-term), check box A, B, C, G, H, or I as it applies to your circumstances.

If you received a 1099-DA, you must check whether your cost basis was included (and that it's correct). If your cost basis is missing, check box H. If your 1099-DA is correct, check box G. If you did not receive a 1099-DA, check box I.

For part 2 (long-term), check box D, E, F, J, K, or L, as it applies to your circumstances.

If your cost basis is missing, check box K. If your 1099-DA is correct, check box J. If you did not receive a 1099-DA, check box L.

If you're generating your 8949 forms using Koinly, you can upload your 1099-DA forms, and it will automatically check these boxes for you. If you have transactions not reported on a 1099-DA from non-custodial wallets, it will automatically default to box I/L.

You do not have to upload your 1099-DAs to Koinly. The likelihood is that your form is incorrect, as exchanges do not have to report cost basis to the IRS in 2026 (for transactions in 2025). As well as this, exchanges will not be penalized for issuing 1099-DAs late for this year, and as a result, some have failed to issue forms so far, so many users may not receive a 1099-DA ahead of the tax deadline.

If this is the case for you, you can request a filing extension, which will automatically give you until October 31 to file, or you can file without your 1099-DA forms (as many users will be at this point).

Koinly Form 8949 example

Your 8949 forms look a little different this year.

You’ll receive an individual 8949 for each exchange/wallet you use. This will be split into short and long-term disposals as required. Each 8949 will have a consolidated summary of transactions, as well as a statement breaking down individual disposals for each exchange.

For centralised exchanges, where you may or may not have received a 1099-DA, you can now check boxes G/H/I (short-term) or H/K/L (long-term) as applicable as to whether your cost basis was or wasn’t reported, or indeed whether you didn’t receive a 1099-DA at all, given that some exchanges have delayed issuing these.

For non-custodial wallets, your Form 8949 will default to boxes I/L (transactions not reported on a 1099-DA).

You can see an example of your form(s) and statements below.

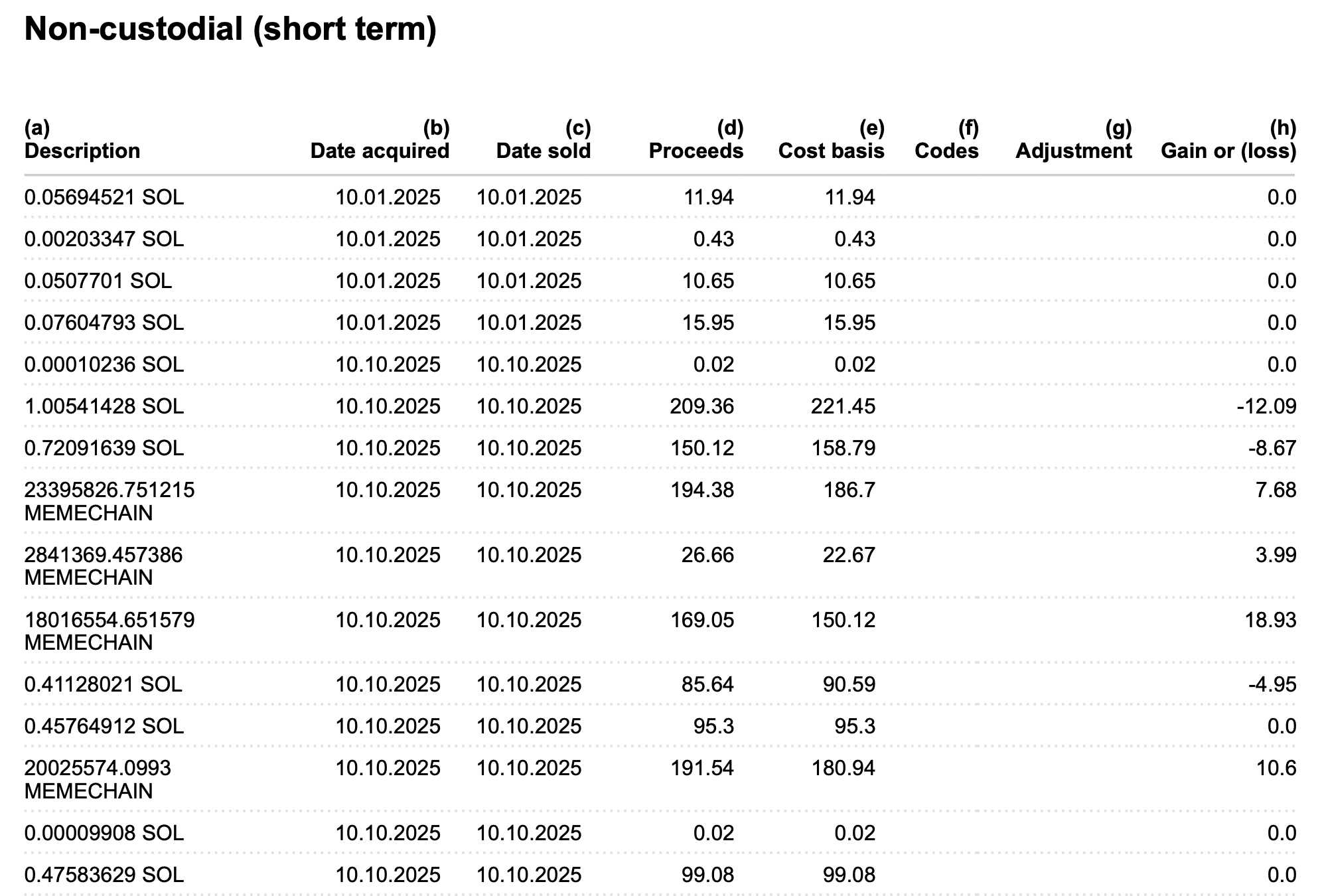

Form 8949 Part 1 (short-term) example

Form 8949 Part 2 (long-term) example

What if I have too many transactions on Form 8949?

Your new 8949 is already aggregated. There is a non-aggregated statement for each wallet/exchange.

Schedule D for crypto net capital gains

Schedule D (Form 1040) is the form you’ll use to report your net capital gain or loss from all investments. This includes your crypto activity, as well as any gains or losses from businesses, estates, and trusts, so you'll need to

Like Form 8949, Schedule D is split into three sections: for your short-term capital gains and losses, your long-term capital gains and losses, and a summary.

For part 1 (short-term capital gains and losses), fill out either line 1a, 1b, 2, or 3. Refer back to the box you checked in Form 8949. If you've uploaded your 1099-DA into Koinly, these will be split for you. If not, it will default to line 3.

Then you'll need to fill out columns D, E, and H.

d) Total proceeds

e) Total cost basis

h) Total gain or loss

You’ll need to fill out the rest of part 1 as it relates to your unique investments, but line 6 (short-term capital loss carryover) is of particular importance to all investors. This is where you report any capital losses you want to carry over, so if you’ve already offset up to $3,000 in capital losses against your gains or your personal income, report any further losses to carry over here.

Once you’ve done this, head to line 7: net short-term capital gain or loss. Report your net capital gain or loss from all investments, including crypto, here.

For part 2 (long-term capital gains and losses), fill out either line 8a, 8b, 9, or 10. Refer back to the box you checked in Form 8949. If you've uploaded your 1099-DA into Koinly, these will be split for you. If not, it will default to line 10.

You'll need to fill out columns D, E, and H:

d) Total proceeds

e) Total cost basis

h) Total gain or loss

Like above, line 14 is where you’ll report any long-term capital loss carryover.

Once you’ve filled this out, go to line 15 to report your long-term net capital gain or loss from all investments, including crypto, here.

Now head to Part 3 (Summary).

On line 16: combine line 7 and line 15 and enter the result into line 16.

The instructions will vary from here depending on whether you have a net capital gain or a net capital loss:

If you have a net capital gain: You also need to fill out lines 17 through 20.

If you have a net capital loss: Skip ahead to line 21.

In either instance, you'll need to report these figures on line 7 of Form 1040.

Schedule 1 for crypto income

Not all of your crypto investments will be viewed as a capital gain or loss. In some instances, your crypto investments will be seen as a kind of income, just like a salary or a bonus (learn more in our guide to crypto taxes).

The form you use to report your crypto income will be either:

Schedule 1 (Form 1040)

Schedule C (Form 1040)

You may or may not need all of these forms. It all depends on the type of crypto transactions you’ve made. We’ll look at each form in turn.

IRS Schedule 1 (Form 1040)

Crypto income, such as staking rewards or airdrops, is generally reported as ordinary income. If earned as part of a business (mining operation, validator services, NFT sales at scale), it belongs on Schedule C. Otherwise, report on Schedule 1 as ‘other income.

You’ll find this in part 1, line 8V.

IRS Schedule C (Form 1040)

If you’re self-employed and earn income through crypto, you should use Schedule C (Form 1040) to report your crypto income. Even if you have a regular job, you might be considered self-employed if you were running a crypto mining operation or other activities at a similar scale.

If your crypto income activities do amount to those of a self-employed taxpayer, you’ll need to fill out Schedule C (Form 1040), as well as pay self-employment taxes. These taxes account for Medicare and Social Security taxes usually accounted for in employee paychecks.

You’ll report your gross income and profit in part 1 of Schedule C.

If you’re seen to be running a business, you can also deduct any expenses related to the business (like mining equipment) in line 30, part 2 of Schedule C.

How to report virtual currency on your individual tax return (Form 1040)

Last, but by no means least, is Form 1040. This is your Individual Income Tax Return Form.

You’ll need to add all of the forms you’ve completed to your Form 1040.

Then on your Form 1040, you'll need to fill out the following lines as they relate to your previous forms.

On line 7A report your net capital gain or loss from Schedule D. Fill 7B as applies to your circumstances.

You'll also need to check the box: "At any time during 2025, did you (a) receive (as a reward, award, or payment for property or services); or (b) sell, exchange, gift, or otherwise dispose of a digital asset (or a financial interest in a digital asset)?"

Fill out the rest of Form 1040 as it relates to your individual circumstances. Once you’ve completed Form 1040, you’re done! You just need to ensure you’ve submitted these forms to the IRS before April 15.

Attach all these forms to their Individual Income Tax Return Schedule 1 (Form 1040) by April 15.

Key changes for the 2026 tax season

There are two important changes you need to know about for the 2025 financial year, ahead of the 2026 tax reporting season:

Form 1099-DA: Starting in the 2025 tax year (filed in 2026), crypto exchanges, brokers, and some payment platforms will issue Form 1099-DA to report digital asset transactions. Similar to how brokers issue Form 1099-B for stocks, this new form will standardize how crypto proceeds, sales, disposals, and certain income events are reported to the IRS. U.S. taxpayers with reportable digital asset activity on covered platforms will receive it, and the IRS will receive a direct copy as well. This matters because any discrepancies between your tax filing and the IRS’s copy of Form 1099-DA could trigger a CP2000 under-reporting notice or even an audit. To avoid issues, taxpayers should reconcile their personal transaction records with the 1099-DA they receive, making necessary adjustments on Form 8949 (such as for fees, transfers, or cost basis mismatches).

Rev. Proc. 2024-28: In 2024, the IRS released Revenue Procedure 2024-28, which changes how the cost basis for digital assets must be tracked and reported. Previously, many investors used a universal pooling method across wallets and exchanges, but the new rules mandate account-based tracking. This means each wallet or exchange account now requires separate tracking of basis and holding periods, making transfers between accounts more complex to allocate correctly.

How to calculate your crypto tax

Before you can report your crypto tax to the IRS, you need to calculate your crypto totals. This means you’ll need to calculate your:

Capital gains from crypto

Capital losses from crypto

Income from crypto

Any expenses relating to your investments

As you can see, reporting your crypto taxes to the IRS can be time-consuming. For investors with many disposals, filling out Form 8949 alone is a huge amount of work, but Koinly can help.

How to report crypto on your tax return with Koinly

If you’re using a crypto tax calculator like Koinly, then calculating your crypto tax liability is a breeze because Koinly is a Form 8949 (and Schedule D) generator for crypto, which can also help you report any crypto income as well.

All you need to do is import your crypto transaction history from your various wallets, exchanges, or blockchains using API or CSV files. Koinly will then calculate your capital gains, losses, income, and expenses. You can also upload your 1099-DA and our software will reconcile this against your data.

Once all your information is imported, head to the tax report page in your Koinly account, where you’ll find a simple summary of your crypto taxes.

Then upgrade to a paid plan and download Form 8949 and Schedule D, with all your capital gains and losses calculated for you. Koinly can also generate the income totals you need for your Schedule 1 form via our Complete Tax Report.

For investors using a third-party service to file their tax report, Koinly can also generate specific reports for TurboTax and TaxAct reports; just upload our report to your chosen tax app.

FAQs

What is a 8949 Form?

Form 8949 is an IRS form that reports disposals of capital assets like stocks or crypto. This form records every single disposal of a capital asset throughout a given financial year, including details like transaction date, amount, cost basis, proceeds, and more. The total capital gains and losses are then consolidated and reported on Schedule D.

What codes for Form 8949?

Column F in Form 8949 refers to codes that relate to specific adjustments to any gain or loss, while Column G is the amount of adjustment. For most transactions, you won't need to enter a code. For some specific transactions where an adjustment is necessary, the codes are as follows:

B: You received a Form 1099-B (or substitute statement) and the basis shown in box 1e is incorrect.

T: You received a Form 1099-B (or substitute statement) and the type of gain (or loss) shown in box 2 is incorrect

N: You received a Form 1099-B or 1099-S (or substitute statement) as a nominee for the actual owner of the property

H:- You sold or exchanged your main home at a gain, must report the sale or exchange on Part II of Form 8949 and can exclude some or all of the gain

D: You received a Form 1099-B (or substitute statement) showing accrued market discount in box 1f

Q: You sold or exchanged QSB stock and can exclude part of the gain

X: You can exclude all or part of your gain under the rules explained in the Schedule D instructions for DC Zone assets or qualified community assets

R: You are electing to postpone all or part of your gain under the rules explained in the Schedule D instructions for any rollover of gain

W: You have a nondeductible loss from a wash sale

L: You have a nondeductible loss other than a loss indicated by code W

E: You received a Form 1099-B or 1099-S (or substitute statement) for a transaction and there are selling expenses or option premiums that aren't reflected on the form or statement by an adjustment to either the proceeds or basis shown

S: You had a loss from the sale, exchange, or worthlessness of small business (section 1244) stock and the total loss is more than the maximum amount that can be treated as an ordinary loss

C: You disposed of collectibles

M: You report multiple transactions on a single row, as described in Exception 2 or Special provision for certain corporations, partnerships, securities dealers, and other qualified entities under Exceptions to reporting each transaction on a separate row, earlier

Z: You are electing to postpone all or part of your gain under the rules explained in the Schedule D instructions for investments in QOFs

Y: You are reporting your gain from a QOF investment that you deferred in a prior tax year

P: You are a nonresident alien individual, foreign trust, foreign estate, or foreign corporation who sold or exchanged an interest in a partnership engaged in a U.S. trade or business

O: You have an adjustment not explained earlier in this column

If you have no adjustments, simply leave Columns F and G blank. If you have multiple adjustments, enter all codes that apply in Column F in alphabetical order and your net adjustment in Column G.

Do you have to report crypto under $600?

Yes. You need to report any capital gains, losses, or income from crypto to the IRS regardless of the amount. The confusion over $600 often comes from exchanges issuing 1099-MISC forms for crypto income over $600 in a given financial year. This form doesn't mean crypto under $600 shouldn't be reported, this is just the threshold at which exchanges are required to issue a 1099-MISC form. You can learn more in our 1099 crypto forms guide.