Crypto Staking Taxes (2026 Guide)

Staking is a great way to earn passive income from your crypto, but the IRS wants its cut. Learn more about crypto staking taxes in our 2026 guide.

Staking rewards are classed as additional income by the IRS and are subject to Income Tax.

Liquid staking may have different tax implications.

Staking rewards are taxable at the point you receive them and have "dominion and control" over them.

You'll also pay capital gains tax on any gain if you later sell, swap, or spend your staking rewards.

Want to learn about crypto staking? Check out our crypto staking guide.

Is crypto staking taxable?

Yes. Generally, the IRS classes staking rewards as ordinary income, as clarified in Rev. Rule 2023-14

However, it matters how you're staking, as the tax implications may vary depending on the specific transaction.

How is crypto staking taxed?

For proof-of-stake mechanisms, staking rewards are ordinary income and subject to income tax. This applies whether you're using a centralized exchange or a non-custodial wallet.

But there are other kinds of staking, as well as nuances like lockup periods, that impact the tax treatment.

At what point are staking rewards taxable?

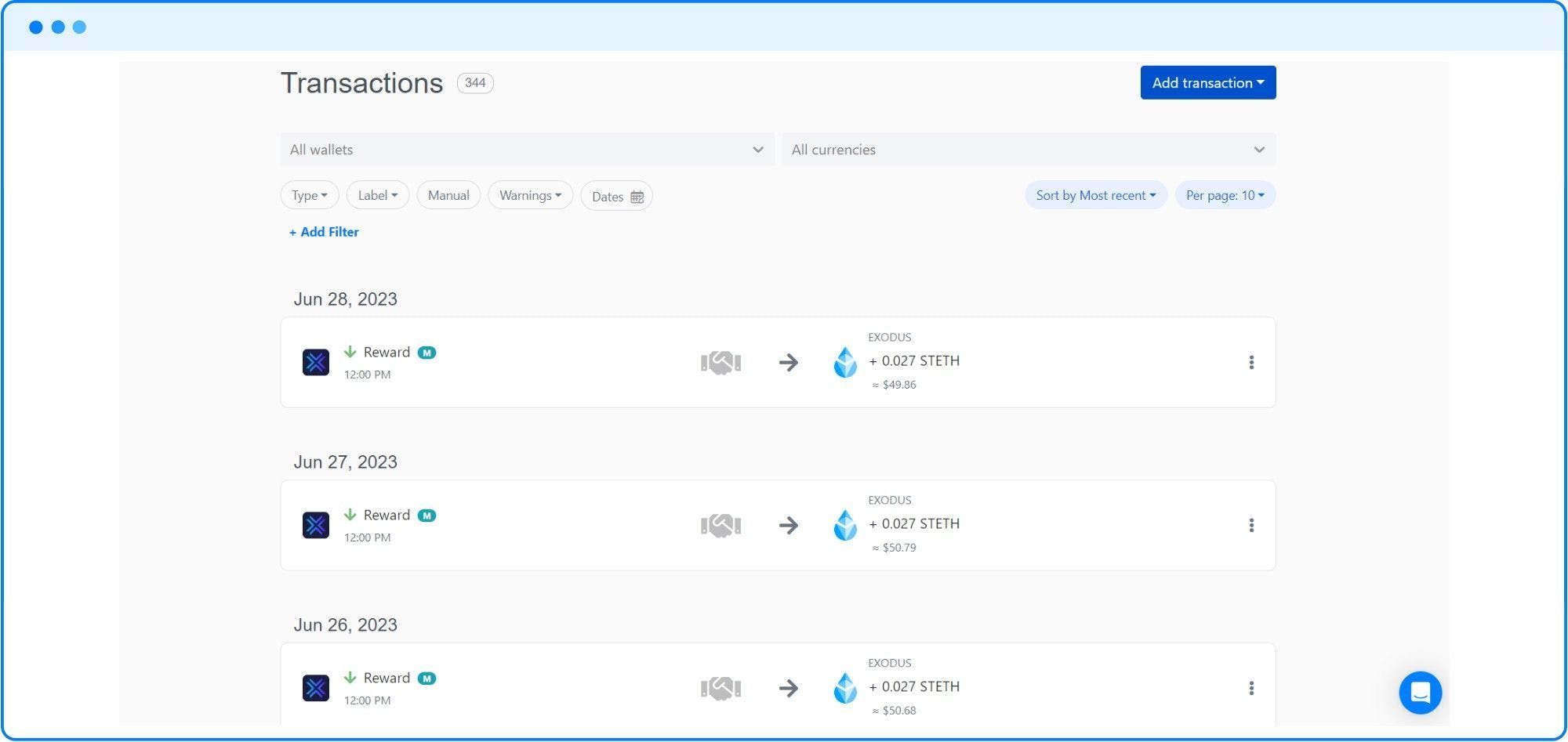

Some staking rewards, like ETH2, are locked up for a given period of time. So while you may accrue staking rewards, you can't access them until the lockup period has expired. This matters for taxation because it isn't until the point you have "dominion and control" over your staking rewards that they're taxable. In other words, it isn't until you can actually sell or trade your staking rewards that the taxable event occurs in these instances.

If there is no lockup period, your staking rewards are taxable as soon as you receive them.

How is liquid staking taxed?

Some investors opt to use protocols like Lido or Rocket Pool to earn staking rewards without losing liquidity while their asset is staked. In these instances, you'll generally receive a token representing your staked asset. For example, if you stake ETH on Lido, you'll receive stETH. This may be a trade, and therefore a taxable disposal, and subject to capital gains tax.

When it comes to your rewards, the tax implications depend on the protocol and how your rewards are distributed. In some instances, the value of your token will increase. In others, you'll receive rewards in the form of more tokens. For the latter, receiving new tokens will be classed as ordinary income. For the former, there is no tax liability until the point you dispose of the token (by selling or trading it) and realise your rewards as a capital gain, which would be subject to capital gains tax.

How is DeFi staking taxed?

DeFi staking can refer to a huge variety of protocols, but what matters is the specific transaction.

If you're earning new tokens in your DeFi staking, this is likely to be classed as ordinary income and subject to income tax.

Meanwhile, if you're trading tokens for your staked asset, this is more akin to a crypto-to-crypto trade, and any capital gain would be subject to capital gains tax.

How is NFT staking taxed?

If you earn rewards from staking NFTs, these will generally be classed as ordinary income and subject to income tax.

How are staking pools taxed?

Earning staking rewards via a staking pool is generally classed as ordinary income and subject to income tax, even if you do not withdraw your rewards, provided you have the ability to withdraw them.

Depositing and withdrawing crypto from a staking pool is likely not considered a taxable event, much like a transfer. The exception to this would be if you received a token representing your asset in the staking pool in return, in which case this may be a taxable disposal under capital gains tax.

Are crypto staking rewards double-taxed?

Yes, crypto staking rewards may be taxed twice, but it won't be on the same profits.

You'll pay income tax based on the FMV value in USD upon receipt. If you later dispose of your staking rewards, you'll pay capital gains tax on any gain.

Example

You receive 0.5 ETH in staking rewards.

The FMV of your 0.5 ETH is $1,000, and you'll pay income tax on this. This will also be your cost basis for your 0.5 ETH.

You later sell your 0.5 ETH for $1,500. To calculate your gain/loss, subtract your cost basis from your sale price:

$1,500 - $1,000 = $500.

You'll pay capital gains tax on $500.

How do other countries tax crypto staking rewards?

Generally, in a similar way to the IRS, although a couple (like the CRA in Canada) haven't released as clear guidance.

In the UK & Australia, crypto staking is also ordinary income upon receipt. Meanwhile, some countries like Austria differentiate between staking directly and staking via a third party, with the former being tax-free and the latter being ordinary income.

How to calculate staking rewards

Calculating staking rewards is easy. Just identify the fair market value (FMV) of your staking rewards in USD on the day you received them.

So, for example, if you earn 0.2 ETH a month from staking, identify the FMV of 0.2 ETH in USD on each date you received ETH throughout the financial year.

If you've sold or traded your staking rewards, you'll also need to calculate whether you have a capital gain or loss, and pay capital gains tax on any subsequent gain.

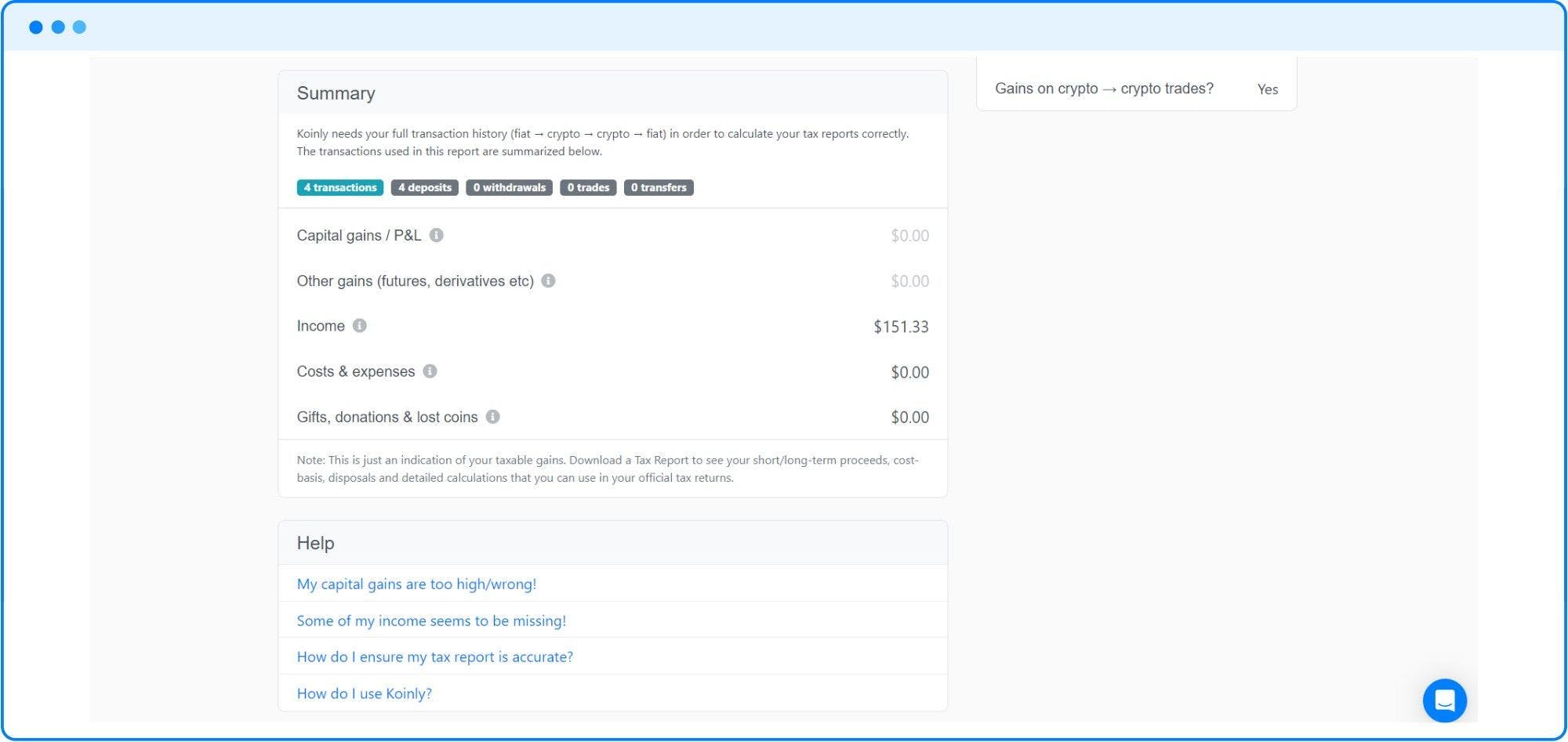

Obviously, this can be time-consuming given the price fluctuations of crypto throughout the year, which is why most investors opt to use a crypto tax calculator like Koinly.

Are my staking rewards reported to the IRS?

In some instances, yes. If you've staked using a centralized exchange like Coinbase or Kraken, your staking rewards may be reported to the IRS on Form 1099-MISC. This generally only applies if you have more than $600 in rewards throughout the financial year.

How to report crypto staking rewards on taxes

You report staking rewards on your annual tax return on Schedule 1 or Schedule C, depending on your employment status.

You'll report the total income from staking for the financial year in USD. Any capital gains/losses related to staking activities go on Form 8949 and Schedule D.

How Koinly can help

It's easy to track with a crypto tax calculator like Koinly, with automatic and manual tagging of staking rewards.

In most instances, Koinly is pretty smart and will automatically recognize and tag staking transactions. But don't worry if not, you can also manually tag your transactions to get a perfectly accurate tax report.

Once Koinly has calculated the fair market value of your staking rewards in your chosen fiat currency, you can simply download the reports you need and file them with the IRS. You can even see a preview of your taxable income from crypto in your tax summary.

Learn more about how staking works in Koinly in our help guide, or sign up and try Koinly free today.

FAQs

Do I have to pay tax if I sell my staking rewards?

Yes. Selling crypto, including staking rewards, is a disposal of an asset, and any gain is subject to capital gains tax. You'll use the fair market value of your staking rewards at the point you receive them as your cost basis.

Are staking expenses tax deductible?

This all depends on how you're viewed, but if you're seen to be operating a business in the course of your staking activities, you would be able to deduct this from your taxes.

Which IRS form do I report staking rewards on?

This depends on your employment status. Salaried employees should report income from staking rewards as "other income" on Form 1040 Schedule 1, while self-employed taxpayers should use Schedule C.

What is dominion and control and what does it mean for staking taxes?

Dominion and control are concepts that relate to ownership. For staking, this matters because in many instances, investors don't have the ability to freely withdraw their rewards. The IRS clarified that it isn't until the point that investors have dominion and control over their staking rewards that they're taxable.

How does the Tezos court case impact staking taxes?

In short, it doesn't. The IRS refunded a couple in relation to Tezos staking rewards several years ago. Many investors then assumed that staking rewards were no longer taxable.

However, this is because at the time, the IRS had no guidance on staking rewards. It now does, and that guidance is crystal clear staking rewards are taxable.