Adjusted Cost Basis & Superficial Loss Rule in Canada

Learn everything you need to know about the adjusted cost basis method, the superficial loss rule, and how to stick to the CRA rules when calculating your crypto taxes and tax loss selling in Canada.

Canadian investors must use the adjusted cost basis method when calculating gains and losses from identical capital properties, like crypto.

This method dictates that the average cost of the property is used to calculate a gain or loss.

The superficial loss rule exists to stop investors from creating wash sales through tax loss selling.

This rule discounts any losses as deductible if a similar asset is purchased within a 30-day time period.

What's the adjusted cost basis method?

The CRA says when you're dealing with identical capital properties like crypto, the only allowable accounting method is the Ajdusted Cost Basis method.

This method states that you calculate the average cost of the property to calculate any subsequent gains or losses. To do this, take the total cost of a group of identical crypto assets (i.e., ETH or BTC) and divide it by the number of assets you own.

For example, you own 3 ETH. 2 ETH have an adjusted cost basis of $500, while 1 ETH has an adjusted cost basis of $3,000.

Using the ACB method, you'll add up the total cost of your ETH, so $4,000, and divide this by the total amount of ETH owned, resulting in an average cost basis of $1,333.34. You'll then use this cost basis to calculate any subsequent gains or losses when you dispose of your ETH by selling, swapping, spending, or gifting it.

But there's a problem with the average cost basis method: investors can easily manipulate it to create artificial losses, also known as wash sales.

What is the superficial loss rule?

In theory, investors could simply sell multiple assets at a loss in a given pool and immediately buy them back to create artificial losses to reduce their tax bill. This is what's known as a wash sale, and it's why the CRA has a specific rule to prevent it: the superficial loss rule.

The superficial loss rule prevents investors from deducting artificial losses. It's easier to understand with a tax loss selling example.

Example

It’s close to the end of the tax year, and an investor has so far made substantial capital gains from crypto, which they need to pay tax on.

However, this investor is also holding an asset that has depreciated in value. They want to keep holding this asset (because they believe it will appreciate in value in the long run), but they also want to take advantage of the loss made so far to reduce their capital gains taxes.

So they decide to sell the asset. This is a taxable event that triggers a capital loss that can be allocated against their capital gains for the year, reducing their overall taxes. But because they want to continue holding the asset, they buy it back the next day for the same price they sold it for.

The superficial loss rule prevents the scenario above from creating an unfair tax advantage. The CRA says the superficial loss rule kicks in when both of these conditions are met:

The taxpayer (or someone acting on their behalf) acquires cryptocurrency that is identical to the one that they dispose of, either 30 days before or after the disposal, and

At the end of that period, the taxpayer or a person affiliated with the taxpayer owns or has a right to acquire the identical property.

If an investor meets these conditions, they're unable to offset it against their gains from the year.

Let's take a look at another example to explain where the superficial loss rule would kick in.

EXAMPLE

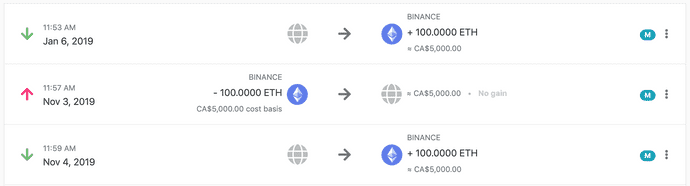

John buys 100 ETH on the 6th of Jan for a total price of $5,000. In November of the same year, he sells them at a loss, for $3,000.

To spare you the math here, we will simply enter these transactions into Koinly which will calculate the gains:

So, John made a loss of $2,000 (who would have guessed?!)

Now, John thinks he is pretty clever so he decides to buy the ETH back the next day (for the same price) but... you guessed it.

The superficial loss rule zeroes out his loss from the previous day.

Basically what has happened is that the $2000 loss John made on the 3rd of November was added to his cost basis for the coins he repurchased the following day. This effectively nullifies any tax advantage that John thought was possible by selling at a loss before quickly rebuying.

In order to avoid the application of the superficial loss rule, John would have to wait 30 days following the sale on the 3rd of November before rebuying his ETH.

Use a crypto tax calculator to stay compliant

A crypto tax calculator like Koinly can help you stay compliant with the CRA rules as it calculates your crypto gains and losses using the adjusted cost basis method, with the superficial loss rule factored in. It also features a tax optimization tool that can help you identify tax loss selling opportunities to reduce your tax bill.

If you’re looking for more general information on crypto taxes in Canada, check out our Crypto Tax Canada Guide.