IRS Crypto Tax Audits: How to Avoid & Prepare

The IRS has increased crypto tax enforcement, including issuing notices to investors and increasing the number of crypto tax audits and a new information request for 2026 that asks for every exchange and wallet ever used. Find out how to avoid a cryptocurrency tax audit, and how to prepare if you're selected for one.

Crypto tax audits are increasing as the IRS enforces crypto tax compliance.

An audit is usually preceded by a notice to declare any crypto profits.

The audit will involve a thorough examination of transaction records and proceeds.

A new 2026 information request asks investors to list every single exchange or wallet they've ever used.

A crypto tax calculator can help you with record-keeping and remaining compliant.

Will the IRS audit you for crypto?

Yes. If the IRS believes you're underreporting or failing to report profits from crypto, they may audit you. This is usually preceded by a notice to warn you to declare any crypto profits.

Why are cryptocurrency tax audits increasing?

The IRS has made it clear that they’re increasing audits on taxpayers involved in crypto. They published information on the ‘tax gap’, stating an estimated $688 billion in tax revenue is lost due to a lack of compliance, and specifically cited crypto as a factor in this.

Since then, the IRS got a huge budget increase ($80 billion!) in order to hire more agents to improve enforcement, including for crypto investors. They’ve also been putting pressure on crypto exchanges operating in the US to share KYC information with John Doe Summons as part of Operation Hidden Treasure.

Audits have since increased, leading to the first conviction for tax evasion related to Bitcoin, where a man was sentenced to two years in prison, plus more than $1 million in restitution.

What's Operation Hidden Treasure?

Operation Hidden Treasure is an enforcement initiative launched in March 2021 by the IRS to identify tax violations relating to cryptocurrency.

As part of this operation, the IRS has utilized John Doe Summons to compel crypto exchanges to share user data. They have won appeals against Coinbase, Kraken, and Poloniex so far.

With the successful summons so far, the IRS has asked for KYC records on individuals engaging in transactions of $20,000 or more in a financial year. For Coinbase specifically, more than 10,000 letters were sent out to Coinbase users, warning them that they had failed to report additional income, and many crypto tax audits arose as a result.

How to avoid a crypto tax audit

You can’t completely remove the possibility of a tax audit, but you can lower the chances of being flagged.

Report crypto accurately

Make sure your tax filing reflects:

Your full history of crypto trades and transfers

The cost-basis method you used (FIFO, LIFO, HIFO)

Any assumptions or gaps in the data

Tracking every transaction can be tough if you use several wallets and exchanges. Koinly can pull your activity from more than 1,000+ platforms to make this easier.

Clarify changes in income

Large drops in income or sudden jumps in expenses can attract attention. Provide supporting documents that explain those shifts.

Double-check your tax return

Simple mistakes can raise your audit risk. If you had a high volume of crypto trades, go over your numbers thoroughly and review the data, whether you're using a tax calculator or doing it yourself.

Be cautious with deductions

If you operate a crypto-related business, like mining, you can deduct legitimate expenses. Just avoid claiming deductions that seem disproportionate to your earnings. Keep organized records of every cost in case the IRS asks for proof.

How do I know if I'm going to be audited?

Most people learn that an IRS crypto audit is on the way when they receive an official notice. Since 2019, the IRS has issued three main letter types:

6174: A general reminder that crypto is taxable and must be reported.

6174-A: A stronger warning stating that enforcement is possible if your filings appear incomplete.

6173: A notice sent to taxpayers whom the IRS suspects of underreporting. It includes a response deadline and requires proof of proper reporting or an amended return.

Anyone receiving any of these letters should assume an audit is possible.

Even without a letter, or even if you didn’t use an exchange targeted by IRS summonses, the agency can still review your crypto activity. The virtual asset question on your tax return is often enough to prompt a deeper look, especially if your financial records don’t line up with your reported income.

Types of crypto tax audits

The IRS handles crypto audits the same way it handles regular tax checks. If you trade or invest in crypto, you might run into one of these:

Correspondence audit: The IRS mails a request for more details or proposes changes to your return.

Office audit: You’re asked to meet at a local IRS office to clarify specific issues, often related to crypto gains or mismatched income.

Field audit: Agents visit your home or business to examine your financial records in depth.

Keeping clean records and reporting your crypto activity accurately makes it a lot less likely you’ll deal with any of these.

What does an IRS crypto audit look like?

IRS crypto audit requests can vary regarding the precise questions you’re asked. This said, there are some similarities between all of them. You will be asked to disclose:

All wallet IDs and blockchain addresses

All digital currency exchange accounts and P2P facilitator accounts.

As well as this, for each individual transaction, you’ll need:

The date and time each crypto asset was acquired.

The cost basis and FMV of each crypto asset at the point of acquisition.

The date and time each crypto asset was sold or otherwise disposed of.

The sale price or FMV of each crypto asset at the point of sale or disposal.

An explanation of the cost basis accounting method used for each crypto transaction.

See an example from Reddit of the type of information requested in a crypto tax audit:

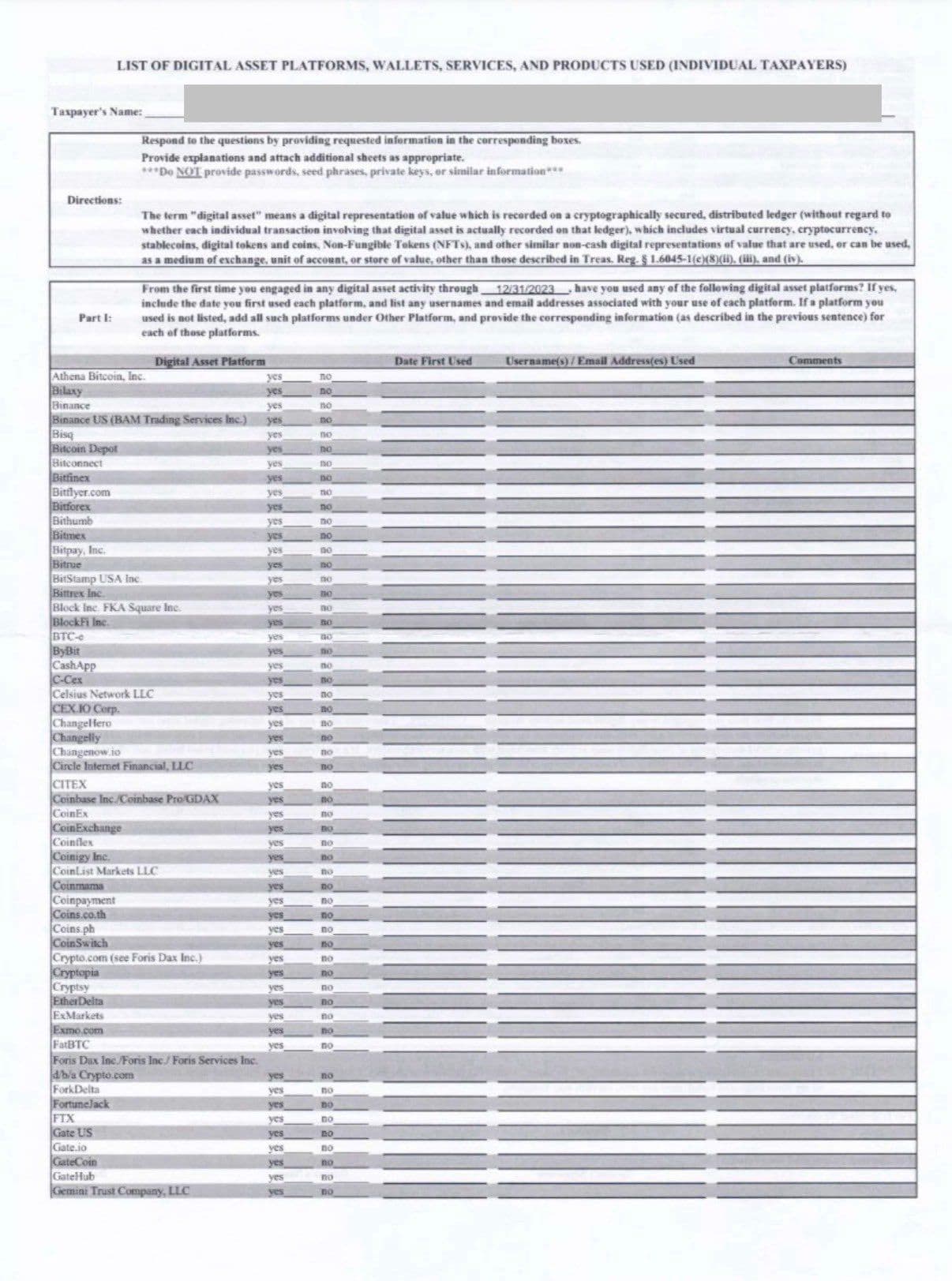

What's the new IRS cryptocurrency information request?

There's a new information request form from the IRS in 2026, that asks taxpayers to disclose their entire history with exchanges and wallets.

This new form is structured in three parts

The first section lists over 100 centralized exchanges (such as Coinbase, Binance, Kraken, and others) and requires you to indicate whether you used each one, when you first used it, and what account identifiers (emails or usernames) were associated with it. The disclosure period is not limited to the tax years under audit; it asks about crypto activity going back to your very first involvement with crypto.

The second section focuses on self-custody wallets and DeFi tools (e.g., MetaMask, Ledger, Trezor), asking whether they were used, when they were first used, what blockchains were involved, and what type of activity occurred.

The third section requires the recipient to certify the answers under penalty of perjury.

Due to the third section in particular, it's adviseable that anyone who receives this form speaks with an experienced crypto accountant or attorney.

How long does an IRS crypto audit take?

It varies. If your crypto activity is simple, just a few exchanges and basic trades, the audit usually moves quickly.

If you’ve got thousands of trades or more complex activity (staking, yield farming, liquidity mining, etc.), expect it to take longer.

The examiner will review the documents they requested, loop in crypto specialists if needed, and follow up with more questions if something doesn’t add up. When the audit wraps, you’ll get a letter with the results and any tax you may owe. You typically have 30 days to appeal. Cases involving suspected fraud can be sent to the Department of Justice.

How far back can tax audits go?

Normally, the IRS looks at the past three years.

If they suspect major mistakes, they can go back six years.

If they think a return was fraudulent—or not filed at all—there’s no time limit.

For crypto investors, that means keeping solid records for every year you trade. A tracking tool like Koinly makes this a lot easier.

How to prepare for an IRS audit

Getting ready for a crypto audit isn’t complicated—you just need clean records and clear explanations. Here’s what to focus on:

Gather your transaction history: Pull every trade, transfer, deposit, and withdrawal from all exchanges, wallets, and blockchains you’ve used. Make sure the data covers the full audit period.

Reconcile your numbers: Match your transaction records with what you reported on your tax return. Fix gaps, duplicates, or missing cost basis before the IRS points them out.

Document your methods: Have notes on the cost-basis method you used (FIFO, LIFO, HIFO), how you valued tokens, and any assumptions you made when data was incomplete.

Keep proof of income and expenses: Store receipts, screenshots, CSV files, mining or staking payout logs, and anything else that backs up your reported income or deductions.

Prepare explanations for unusual activity: Large losses, sudden jumps in income, or heavy transaction volume may prompt questions. Be ready to explain them clearly.

Stay organized: Sort everything by year and exchange/wallet. When the IRS asks for something, you want to hand it over quickly.

Use crypto tax software (or an expert): Tools like Koinly can help recreate accurate records. If your situation is messy or high-volume, consider bringing in a crypto-savvy tax pro.

Being prepared doesn’t guarantee a smooth audit—but it makes the process faster, less stressful, and far more likely to end without issues.

Should I speak to an accountant?

Yes, if you're facing a crypto tax audit, you should speak to an accountant.

Crypto tax in the US is complicated, and the taxation of many transactions is unclear. While a crypto tax calculator can help with record keeping and calculation, it is not tax advice. You can use our accountant directory to find crypto accountants.

Want an easier way to track crypto taxes?

Staying audit-ready is simple when your records are accurate and complete. Koinly helps you do that by syncing all your wallets, exchanges, and blockchains through API or CSV. It pulls in your full transaction history and automatically tracks gains, losses, income, and expenses, all shown in your dashboard and tax summary.

When it’s time to file, you can download the exact forms you need. For U.S. users, that includes Form 8949, Schedule D, Schedule 1, and reports for apps like TurboTax and TaxAct.

If you ever face an IRS audit, you can export a range of reports to show your complete transaction history and calculations.